by

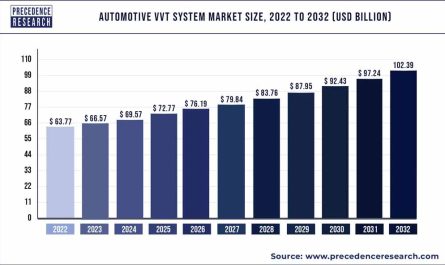

by The global automotive suspension market size is projected to hit US$ 70.19 billion by 2032 from an estimated US$ 50 billion in 2022 with a growing CAGR of 3.5% from 2023 to 2032.

The global automotive suspension market is expected to expand significantly during the forecast period. The suspension systems in automobiles are critical components that help to avoid damage to vehicle components while also allowing for safe and comfortable driving. The changing consumer habits, technical developments, and rising urbanization have all aided the automobile industry’s expansion. The suspension systems for automobiles are constantly improving in order to provide a batter ride experience and greater vehicle road holding capabilities.

Get the Report Sample Copy@ https://www.precedenceresearch.com/gtm-stratergy/1482

The automotive suspension market is likely to be driven by rising vehicle demand in developing regions. In addition, the increased demand for vehicle performance and comfort is likely to drive the market expansion. The lack of standardization and high cost of independent automotive suspension systems may stifle the automotive suspension market growth. The demand for personal automobiles is growing, and independent suspension systems may offer growth potential.

Scope of the Automotive Suspension Market

| Report Coverage | Details |

| Market Size in 2023 | USD 51.5 Billion |

| Market Size by 2032 | USD 70.19 Billion |

| Growth Rate from 2023 to 2032 | 3.5% |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Europe |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Segments Covered | System Type, Region |

| Companies Mentioned | Tenneco Inc., Continental AG, ZF Friedrichschafen AG, Schaeffler AG, Sogefi SpA, Magneti Marelli SpA, KYB Corporation, ThyssenKrupp AG, Mondo Corporation, BENTELER International AG |

Report Highlights

- Based on the suspension type, the MacPherson strut segment dominated the global automotive suspension market in 2020 with highest market share. The MacPherson strut decreases the cost and weight of the architecture by eliminating the need for a separate upper control arm.

- Based on the vehicle type, the passenger vehicle segment is estimated to be the most opportunistic segment during the forecast period. The suspension system is one of the most important components of any vehicle. As a result, the increase of the suspension system is proportional to the volume of passenger vehicles produced.

Regional Snapshot

Asia-Pacific is the largest segment for automotive suspension market in terms of region. This is attributed to an increase in the need for commercial vehicles and improved automobiles and cabs facilities for locals. Also, the expanding population and developing economies of the Asia-Pacific region, which would contribute to the fastest growth of the market.

Europe region is the fastest growing region in the automotive suspension market. This is due to the presence of large number of automobile and components manufacturers. To promote the automotive industry in the Europe, the government entities are developing supportive policies and regulatory frameworks.

Market Dynamics

Drivers

Rise in production of vehicles

Due to their numerous advantages over gasoline-powered vehicles, electric vehicle demand and production have increased dramatically in recent years. Because oil and air filters, fan belts, timing belts, head caskets, and spark plugs do not need to be replaced, fuel-powered vehicles are more cost-effective and efficient. As a result, electric vehicles are rapidly replacing gasoline-powered vehicles as the preferred mode of transportation, limiting the growth of the gasoline-powered vehicle industry. Furthermore, because of improved vehicle dynamics and traction control, automakers are focusing on the development of electric vehicles with the automotive suspension system. As a result, the automotive suspension market is expected to expand due to increased production of electric vehicles.

Restraints

High maintenance costs

The high initial cost of installing new suspension systems raises vehicle prices, which is expected to stymie the growth of the automotive suspension market. The prospect of providing premium features in vehicles incurs additional costs to consumers in the form of hardware, applications, and telecom service charges, limiting market growth. Furthermore, due to the numerous components and sensors, such vehicles are difficult to service and require skilled workers. Vehicle service life is reduced due to the complex structure of systems. As a result, the global automotive suspension market’s growth is expected to be hampered by high initial costs and a complex structure.

Opportunities

Rise in demand for light weight automotive suspension system

The suspension plays an important part in vehicle elegance and comfort, as well as eliminating cabin vibrations. Steel or steel alloys, including stainless steel and carbon steel, are used to create traditional suspension components. These materials, on the other hand, are heavier and have lower strength than other materials. As a result of technological breakthroughs in the automotive industry, automotive lightweight materials such as aluminum, carbon fiber, and titanium alloys have been developed for use in the fabrication of suspension system components. Due to its increased qualities, such as low weight, high specific stiffness, corrosion resistance, capacity to construct complicated geometries, high specific strength, and high impact energy absorption, these materials are utilized to manufacture suspension components.

Challenges

Lack of standardization

As there will be particular suspension types for each model, the standardization of suspension systems by vehicle type will aid Tier 1 and component manufactures in producing suspension systems in large volumes, lowering overall manufacturing costs. While negotiating supply contracts, original equipment manufacturer (OEMs) and suspension suppliers can develop standardization for independent suspension in terms of key characteristics. For both OEMs and suspension suppliers, this might be a win-win situation. Thus, the lack of standardization is a huge challenge for the growth of automotive suspension market.

Some of the prominent players in the global automotive suspension market include:

- Tenneco Inc.

- Continental AG

- ZF Friedrichschafen AG

- Schaeffler AG

- Sogefi SpA

- Magneti Marelli SpA

- KYB Corporation

- ThyssenKrupp AG

- Mondo Corporation

- BENTELER International AG

Segments Covered in the Report

By Suspension Type

- Macpherson Strut

- Multilink Suspension

- Air Suspension

By System Type

- Passive Suspension

- Semi Active Suspension

- Active Suspension

By Actuation Type

- Hydraulically Actuated Suspension

- Electronically Actuated Suspension

By Vehicle Type

- Passenger Vehicle

- Light Commercial Vehicle

By Geography

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Latin America

- MEA

- Rest of the World

Contact Us:

Mr. Alex

Sales Manager

Call: +1 9197 992 333

Email: sales@precedenceresearch.com

Web: https://www.precedenceresearch.com

Blog: https://www.expresswebwire.com/