by

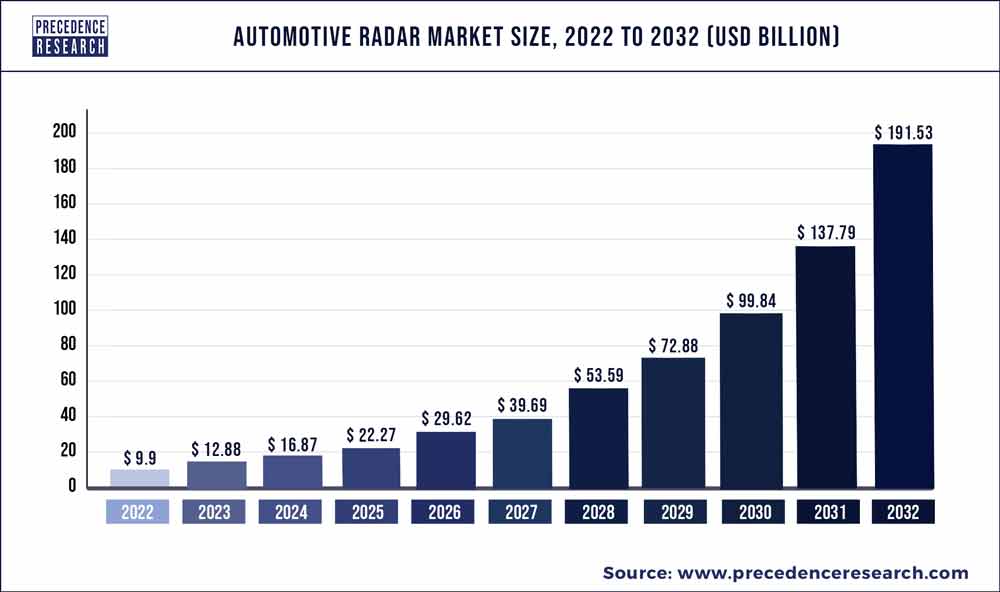

by The global automotive RADAR market size was valued at USD 9.90 billion in 2022 and is expanding to reach USD 191.53 billion by 2032, with a CAGR of 35% from 2023 to 2032.

Key Points

- Asia Pacific led the global market with the highest market share in 2022.

- Europe is predicted to expand at the fastest CAGR during the forecast period.

- By Range, the Short & Medium Range RADAR (S&MRR) segment has held the largest market share in 2022.

- By Application, the intelligent park assist segment generated over 52% of revenue share in 2022.

- By Application, the adaptive cruise control (ACC) segment is expected to expand at the fastest CAGR over the projected period.

The automotive RADAR market has witnessed significant growth in recent years, driven by the increasing demand for advanced driver assistance systems (ADAS) and autonomous vehicles. RADAR (Radio Detection and Ranging) technology plays a crucial role in enhancing vehicle safety by providing accurate detection and tracking of objects, including vehicles, pedestrians, and obstacles, in various driving conditions. As automotive manufacturers continue to prioritize safety and regulatory bodies impose stringent safety standards, the adoption of RADAR systems is expected to escalate further. This introduction sets the stage to explore the dynamics, trends, and competitive landscape of the automotive RADAR market.

Get a Sample: https://www.precedenceresearch.com/sample/1034

Drivers

Several factors are propelling the growth of the automotive RADAR market. Primarily, the rising concern for road safety and the increasing number of road accidents globally have driven the adoption of RADAR-based safety systems. RADAR technology offers reliable performance in adverse weather conditions and low visibility scenarios, making it indispensable for enhancing driver awareness and preventing collisions. Additionally, the growing inclination towards autonomous driving technology, coupled with regulatory mandates requiring the integration of advanced safety features, has boosted the demand for RADAR systems in vehicles. Furthermore, advancements in RADAR technology, such as the development of high-resolution and long-range sensors, are expanding the scope of applications beyond traditional safety functions, including adaptive cruise control and automated parking systems.

Trends:

In the automotive RADAR market, several notable trends are shaping the industry landscape. One prominent trend is the integration of RADAR sensors with other sensing technologies, such as LiDAR (Light Detection and Ranging) and cameras, to create multi-sensor fusion systems. This fusion enhances the overall perception capabilities of ADAS and autonomous driving systems, enabling more accurate object detection and classification. Another emerging trend is the miniaturization of RADAR modules, driven by advancements in semiconductor technology and manufacturing processes. Smaller, more compact RADAR sensors facilitate easier integration into vehicles and enable seamless incorporation into various vehicle designs. Additionally, there is a growing emphasis on the development of automotive-grade RADAR systems that meet the stringent reliability and durability requirements of the automotive industry, ensuring consistent performance over the vehicle’s lifespan.

Automotive RADAR Market Scope

| Report Highlights | Details |

| Market Size by 2032 | USD 191.53 Billion |

| Growth Rate from 2023 to 2032 | CAGR of 35% |

| Largest Market | Europe |

| Fastest Growing Market | Asia Pacific |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Segments Covered | Frequency, Range, Vehicle Type, Application, Regional Outlook |

SWOT Analysis

- Strengths: The strengths of the automotive RADAR market lie in its proven effectiveness in detecting objects in diverse environmental conditions, including rain, fog, and darkness. RADAR technology also offers high accuracy and reliability, making it a preferred choice for safety-critical applications. Moreover, the increasing regulatory push for vehicle safety standards provides a favorable environment for market growth.

- Weaknesses: Despite its strengths, the automotive RADAR market faces challenges related to cost and complexity. High initial investment and integration costs pose barriers to adoption, particularly for smaller automotive manufacturers. Additionally, RADAR systems may experience interference from other electronic devices and environmental factors, affecting their performance.

- Opportunities: The automotive RADAR market presents several opportunities for expansion, driven by the growing demand for advanced driver assistance features and autonomous driving technology. As consumers become more accustomed to technology-driven safety features, there is a rising willingness to pay for RADAR-equipped vehicles. Furthermore, the ongoing research and development efforts aimed at improving RADAR performance and reducing costs create opportunities for innovation and market growth.

- Threats: The automotive RADAR market is susceptible to competitive threats from alternative sensing technologies, such as LiDAR and cameras, which offer complementary capabilities and may gain traction in certain applications. Additionally, regulatory changes and geopolitical factors could impact market dynamics, including trade policies affecting the supply chain and market access.

Segments:

The automotive RADAR market can be segmented based on frequency band, range, vehicle type, and application. Frequency band segmentation includes S-band, C-band, and X-band RADAR systems, each offering different performance characteristics and suitability for various applications. Range segmentation categorizes RADAR systems into short-range, medium-range, and long-range sensors, depending on their detection capabilities. Vehicle type segmentation encompasses passenger vehicles, commercial vehicles, and electric vehicles, each with distinct requirements and adoption trends. Application segmentation covers various ADAS functions, including collision avoidance, blind-spot detection, lane departure warning, and autonomous emergency braking.

Read Also: Automotive LiDAR Market Size To Hit USD 7.43 Billion by 2032

Competitive Landscape:

The automotive RADAR market is characterized by intense competition among key players, including automotive OEMs, Tier-1 suppliers, and specialized RADAR manufacturers. Major companies such as Continental AG, Robert Bosch GmbH, Aptiv PLC, and Denso Corporation dominate the market, leveraging their technological expertise and extensive industry experience to offer innovative RADAR solutions. These companies focus on strategic initiatives such as product development, partnerships, and mergers and acquisitions to strengthen their market position and expand their product portfolios. Additionally, the market landscape features a mix of established players and emerging startups, fostering competition and driving technological advancements in automotive RADAR systems.

Some of the prominent players in the automotive RADAR market include:

- Continental AG

- Autoliv Inc.

- DENSO Corporation

- Delphi Automotive Company

- NXP Semiconductors

- Texas Instruments

- Robert Bosch GmbH

- ZF Friedrichshafen

- Valeo

- Analog

Segments Covered in the Report

By Frequency

- 24 GHz

- 77 GHz

- 79GHz

By Range

- Short & Medium Range RADAR (S&MRR)

- Long Range RADAR (LRR)

By Vehicle Type

- Commercial Vehicle

- Passenger Vehicle

By Application

- Autonomous Emergency Braking (AEB)

- Adaptive Cruise Control (ACC)

- Forward Collision Warning System

- Intelligent Park Assist

- Blind Spot Detection (BSD)

- Others ADAS Applications

By Regional Outlook

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of the World

Contact Us:

Mr. Alex

Sales Manager

Call: +1 9197 992 333

Email: sales@precedenceresearch.com

Web: https://www.precedenceresearch.com

Blog: https://www.expresswebwire.com/

Blog: https://www.uswebwire.com/