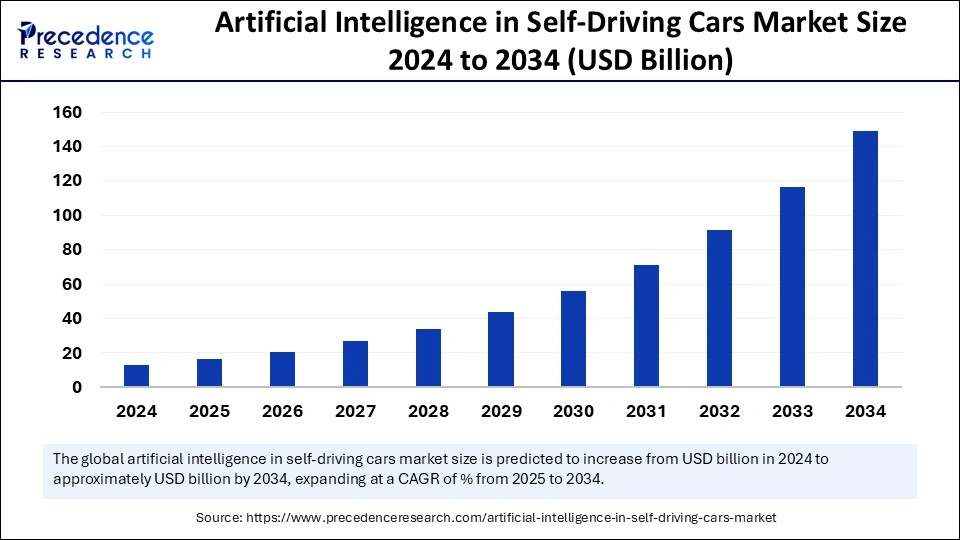

by

by The Artificial Intelligence in Self-Driving Cars Market is multi-dimensional, encompassing hardware components such as GPUs and AI accelerators, software systems for perception and planning, and communication technologies like 5G and Vehicle-to-Everything (V2X). These elements collectively empower vehicles to sense, analyze, and act in real time. The software segment includes algorithms for perception (e.g., object and event detection), prediction (e.g., traffic flow and behavioral modeling), and planning (e.g., path optimization and obstacle avoidance). The hardware segment, on the other hand, comprises powerful processors, LiDAR sensors, radar systems, and high-resolution cameras that feed critical data to the vehicle’s central AI engine.

At the core of these systems lies sensor fusion—a technique that blends data from various sources to create a unified understanding of the environment. This synergy is essential for accurate localization, threat assessment, and decision-making. Machine learning algorithms continuously improve driving models by learning from data captured during both simulations and real-world driving. Computer vision enables vehicles to interpret visual information like road signs, traffic signals, and unexpected hazards, while reinforcement learning allows vehicles to optimize decision-making based on environmental feedback. The market is transforming how vehicles behave, communicate, and navigate, creating a paradigm shift in how people and goods are transported.

Key Market Takeaways

- North America led the global artificial intelligence in the self-driving cars market in 2024.

- Asia Pacific is estimated to expand at the fastest CAGR between 2025 and 2034.

- By vehicle type, the passenger vehicles segment captured the largest market share in 2024.

- By vehicle type, the commercial vehicles segment is expected to expand at a significant CAGR over the projection period.

- By application, the driver assistance systems segment captured the largest market share in 2024.

- By application, the autonomous navigation segment is expected to expand at the fastest CAGR during the forecast period.

Market Dynamics

Market Drivers

A significant driver for this market is the increasing demand for ADAS and intelligent safety systems. Consumers are prioritizing vehicles that offer safety features powered by real-time AI analytics. The integration of 5G and V2X technology further amplifies AI’s capabilities by enabling low-latency communication between vehicles, infrastructure, and pedestrians. This interconnectedness helps mitigate traffic congestion, reduce accidents, and enable cooperative mobility.

Furthermore, the market is experiencing a surge in R&D investment from both automotive giants and technology companies. For example, Tesla’s Dojo AI training supercomputer and NVIDIA’s Drive AGX platforms are pushing the boundaries of real-time decision-making. The expansion of Mobility-as-a-Service (MaaS) platforms is another growth catalyst, as fleet operators seek AI-driven tools for route planning, energy optimization, and predictive maintenance.

AI’s application in security and surveillance vehicles is also growing. Autonomous patrol vehicles, particularly in regions like Dubai, are being equipped with AI systems to ensure public safety, patrol restricted zones, and communicate with central command centers—broadening the application base for AI in vehicles beyond traditional transportation.

Market Restraints

Despite the promise, the market faces significant challenges, most notably cybersecurity and data privacy issues. As vehicles become more connected, they also become more vulnerable to hacking, data breaches, and software manipulation. Real-world examples, such as the Kia portal vulnerability, underscore how even minor software flaws can become critical threats in an autonomous ecosystem.

Regulatory uncertainty is another roadblock. Varying international standards, slow-moving legislation, and public distrust in self-driving technology are delaying market scalability. High-profile incidents involving autonomous vehicles—especially those leading to fatalities—have highlighted the gap between technological capabilities and societal readiness. Moreover, geopolitical tensions and debates surrounding cross-border data flow add another layer of complexity to deploying AI-based autonomous systems at scale.

Market Opportunities

Robotaxis and autonomous ride-hailing services present lucrative opportunities. Companies like Zoox and Cruise are piloting robotaxi programs in major urban areas, with promising results in reducing wait times and lowering operational costs. AI plays a central role in orchestrating fleet movements, ensuring safety, and managing energy consumption.

AI is also transforming fleet management through predictive diagnostics. By analyzing vehicle data, AI can predict mechanical failures, optimize maintenance schedules, and extend vehicle life cycles. Strategic partnerships are accelerating innovation: May Mobility is integrating AI in public shuttles, Wayve has partnered with Microsoft to develop cloud-based training infrastructure, and NVIDIA’s March 2025 alliance with Nexar aims to bring real-time AI vision to mid-tier AVs.

Technological Advancements

AI’s ability to mimic human cognition is evident in its growing capabilities for decision-making and situational awareness. Algorithms now not only detect obstacles but also understand intent—such as whether a pedestrian is about to cross or a driver is about to change lanes. This contextual understanding is crucial in densely populated areas where split-second decisions can make a difference.

Companies like Waymo are deploying advanced AI models trained on millions of miles of real-world data. Waymo currently operates over 200,000 weekly paid autonomous rides, showcasing the scalability of its AI systems. DeepRoute.ai, on the other hand, focuses on affordability by offering Level 4 AI systems optimized for cost-sensitive markets.

AI is also being integrated into public safety initiatives. The Dubai Police’s deployment of AI-driven autonomous patrol vehicles underscores the technology’s potential in security and surveillance. These vehicles use AI to detect unauthorized entry, assess crowd behavior, and monitor emergency zones, demonstrating the versatility of AI applications beyond personal or commercial mobility.

Read Also: Hybrid Train Market Size to Surpass USD 43.3 Billion by 2034

Vehicle Type Analysis

Passenger vehicles remain the primary segment for AI integration, especially in luxury and premium categories. The inclusion of features like AI-based voice assistants, intelligent infotainment systems, and ADAS is becoming standard. Automakers like BMW, Mercedes-Benz, and Audi are focusing on refining user experience through AI personalization and adaptive learning systems.

In commercial vehicles, the push for automation in logistics and delivery services is creating immense demand for AI solutions. Companies like TuSimple are automating long-haul freight, while Waymo Freight and Amazon/Zoox are investing in last-mile delivery automation. AI enhances route planning, reduces delivery time, and minimizes fuel consumption, thus contributing directly to operational cost savings and sustainability goals.

Application Analysis

ADAS systems continue to dominate the application landscape. These systems rely heavily on AI for real-time data interpretation and decision-making. Features such as automatic emergency braking, blind spot detection, and driver monitoring are being standardized across vehicle classes.

Autonomous navigation is expected to witness the fastest growth due to technological advancements in LiDAR, radar, and camera-based systems. AI enhances sensor integration, making vehicles capable of handling complex urban and highway environments. Deep learning models are enabling AVs to understand context, manage traffic interactions, and navigate dynamic road scenarios with increasing confidence.

Regional Analysis

In North America, especially the U.S., a favorable regulatory environment and access to venture capital have allowed firms like Aurora, Cruise, and Zoox to pilot large-scale AI integration. The U.S. Infrastructure Investment and Jobs Act has allocated $4 billion toward AI-powered transportation infrastructure, further accelerating market maturity.

Asia Pacific is emerging as the fastest-growing market due to urbanization, government support, and domestic production advantages. China’s aggressive 5G-V2X deployment, Japan’s 2030 mobility roadmap, and India’s Smart City initiatives are key growth drivers. OEMs are partnering with AI startups to integrate localized solutions that cater to regional infrastructure and user behavior.

Europe remains a pioneer in regulatory frameworks, focusing on AI ethics, safety, and smart city integration. Germany and the UK are leading investments in cooperative mobility systems, while cities like Paris and Hamburg are testing AI-based traffic coordination platforms. The continent’s commitment to reducing emissions aligns well with the rollout of electric autonomous fleets.

Competitive Landscape

Leading players in the AI self-driving car market span technology companies, traditional automakers, and innovative AV startups. NVIDIA remains a cornerstone provider of AI computing platforms, while Intel’s Mobileye leads in vision-based systems. Tesla continues to push boundaries with its FSD suite, supported by its Dojo supercomputer.

Waymo leads the autonomous service segment with operational fleets in multiple cities. Aurora and Zoox are strengthening their logistics and ride-hailing capabilities. GM’s 2025 collaboration with NVIDIA marks a major milestone in combining robotics and automotive AI. The Nexar-NVIDIA partnership focuses on building real-time AI perception for broad-market AV applications, emphasizing scalability and accessibility.

- Apple Inc.

- Aptiv PLC

- Aurora Innovation, Inc.

- Baidu, Inc.

- BMW Group

- Ford Motor Company (Argo AI)

- General Motors (Cruise)

- Mobileye (Intel Corporation)

- NVIDIA Corporation

- Tesla, Inc.

- Toyota Motor Corporation (Toyota Research Institute)

- Uber Technologies, Inc.

- Volkswagen Group (Autonomous Driving Program)

- Waymo (Alphabet Inc.)

- Zoox (Amazon)

Recent Developments and Future Outlook

Recent months have seen major developments in pilot deployments, funding rounds, and technology rollouts. Zoox initiated real-world operations in Las Vegas, while Baidu’s Apollo Go service expanded to six cities in China. Investment in AI-focused AV startups crossed $1.8 billion globally in Q1 2025, indicating robust investor confidence.

The convergence of AI and MaaS is expected to align with broader sustainability goals, enabling carbon-neutral transportation systems through energy-efficient navigation, autonomous EV fleets, and intelligent traffic orchestration. Future AI systems are likely to move from assistance to full autonomy, supported by advances in neuromorphic computing, quantum AI, and synthetic training environments.